Contents

Pradhan Mantri Jan Dhan Yojana (PMJDY)

Pradhan Mantri Jan Dhan Yojana (PMJDY) is a government-backed financial inclusion initiative in India that was launched on 28 August 2014 by Prime Minister Narendra Modi. The scheme aims to provide financial services to the poor, including bank accounts, insurance, and pensions.

| Headline | Description |

| Pradhan Mantri Jan Dhan Yojana (PMJDY) | A government-backed financial inclusion initiative in India that was launched on 28 August 2014 by Prime Minister Narendra Modi. The scheme aims to provide financial services to the poor, including bank accounts, insurance, and pensions. |

| Objectives | * Provide access to financial services to the poor, including bank accounts, insurance, and pensions. * Promote financial literacy and awareness among the poor. * Reduce poverty and improve the lives of the poor. |

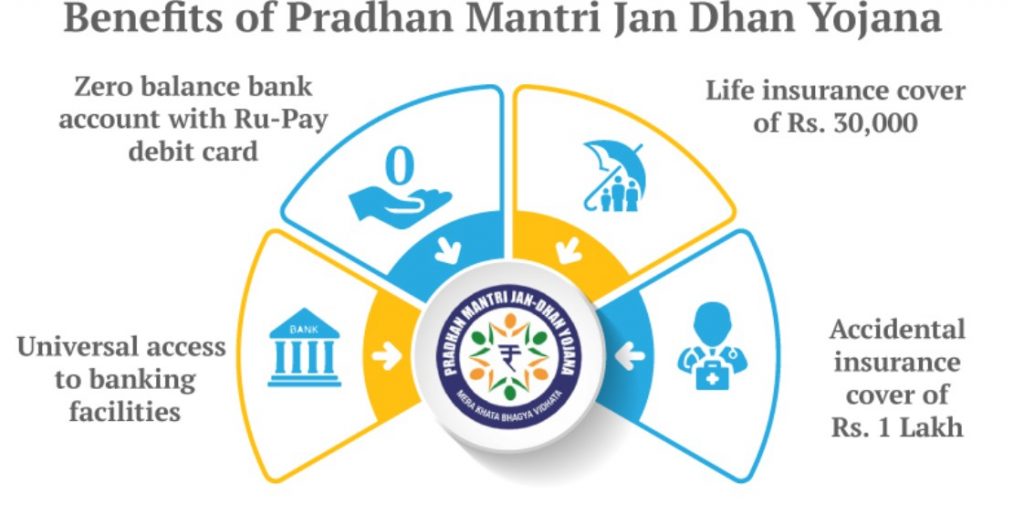

| Benefits | * Access to a bank account with zero balance. * Free accidental death and disability cover of Rs. 2 lakhs. * Free life insurance cover of Rs. 33,000. * Free accidental death and disability cover of Rs. 30,000 for women. * Access to loans at lower interest rates. * Access to government schemes and programs. * RuPay debit card * SMS alerts * Direct benefit transfer (DBT) * Micro insurance * Micro pension |

| Eligibility | * To be eligible for PMJDY, you must be an Indian citizen and you must not have a bank account. You must also meet the following income criteria: * Individual: Up to Rs. 3 lakhs per annum * Joint account: Up to Rs. 6 lakhs per annum * Hindu Undivided Family (HUF): Up to Rs. 12 lakhs per annum |

| How to Apply | * You can apply for PMJDY at any bank branch in India. You will need to provide the following documents: * Aadhaar card * Voter ID card * Proof of residence * Proof of income |

| How to Check Account Balance | * You can check your account balance by using the following methods: * ATM * Mobile banking * Internet banking * SMS |

| How to Withdraw Money | * You can withdraw money from your account using the following methods: * ATM * Bank branch * NEFT/RTGS * IMPS |

| How to Transfer Money | * You can transfer money from your account to another account using the following methods: * NEFT/RTGS * IMPS * Cheque * Demand draft |

| How to Pay Bills | * You can pay bills such as electricity, water, and gas using the following methods: * ATM * Mobile banking * Internet banking * NEFT/RTGS * IMPS |

| Challenges | * Lack of awareness about the scheme. * Lack of infrastructure in rural areas. * Lack of skilled manpower. * Lack of financial literacy among the poor. |

| Future Plans | * The government plans to expand the scope of PMJDY to include more financial services such as credit, insurance, and pensions. * The government also plans to make it easier for people to access the benefits of PMJDY by simplifying the application. |

Objectives

The main objectives of PMJDY are to:

- Provide access to financial services to the poor, including bank accounts, insurance, and pensions.

- Promote financial literacy and awareness among the poor.

- Reduce poverty and improve the lives of the poor.

Benefits

The benefits of PMJDY include:

- Access to a bank account with zero balance.

- Free accidental death and disability cover of Rs. 2 lakhs.

- Free life insurance cover of Rs. 33,000.

- Free accidental death and disability cover of Rs. 30,000 for women.

- Access to loans at lower interest rates.

- Access to government schemes and programs.

Eligibility

To be eligible for PMJDY, you must be an Indian citizen and you must not have a bank account. You must also meet the following income criteria:

- Individual: Up to Rs. 3 lakhs per annum

- Joint account: Up to Rs. 6 lakhs per annum

- Hindu Undivided Family (HUF): Up to Rs. 12 lakhs per annum

How to Apply

You can apply for PMJDY at any bank branch in India. You will need to provide the following documents:

- Aadhaar card

- Voter ID card

- Proof of residence

- Proof of income

How to Check Account Balance

You can check your account balance by using the following methods:

- ATM

- Mobile banking

- Internet banking

- SMS

How to Withdraw Money

You can withdraw money from your account using the following methods:

- ATM

- Bank branch

- NEFT/RTGS

- IMPS

How to Transfer Money

You can transfer money from your account to another account using the following methods:

- NEFT/RTGS

- IMPS

- Cheque

- Demand draft

How to Pay Bills

You can pay bills such as electricity, water, and gas using the following methods:

- ATM

- Mobile banking

- Internet banking

- NEFT/RTGS

- IMPS

Challenges

The main challenges of PMJDY include:

- Lack of awareness about the scheme.

- Lack of infrastructure in rural areas.

- Lack of skilled manpower.

- Lack of financial literacy among the poor.

Future Plans

The government plans to expand the scope of PMJDY to include more financial services such as credit, insurance, and pensions. The government also plans to make it easier for people to access the benefits of PMJDY by simplifying the application process and reducing the documentation requirements.

Overall, PMJDY is a landmark initiative that has the potential to transform the lives of millions of poor people in India. The scheme has already made a significant impact in terms of increasing financial inclusion and promoting financial literacy. The government’s future plans for PMJDY are ambitious and they have the potential to make the scheme even more impactful.

FAQ – Pradhan Mantri Jan Dhan Yojana

What is PMJDY?

PMJDY is a government-backed financial inclusion initiative in India that was launched on 28 August 2014 by Prime Minister Narendra Modi. The scheme aims to provide financial services to the poor, including bank accounts, insurance, and pensions.

Who are eligible for PMJDY?

The following people are eligible for PMJDY:

- Indian citizens

- People who do not have a bank account

- People who have an annual income of up to Rs. 3 lakhs

What are the benefits of PMJDY?

The benefits of PMJDY include:

- Access to a bank account with zero balance

- Free accidental death and disability cover of Rs. 2 lakhs

- Free life insurance cover of Rs. 33,000

- Free accidental death and disability cover of Rs. 30,000 for women

- Access to loans at lower interest rates

- Access to government schemes and programs

- RuPay debit card

- SMS alerts

- Direct benefit transfer (DBT)

- Micro insurance

- Micro pension

How to apply for PMJDY?

You can apply for PMJDY at any bank branch in India. You will need to provide the following documents:

- Aadhaar card

- Voter ID card

- Proof of residence

- Proof of income

How to check account balance?

You can check your account balance by using the following methods:

- ATM

- Mobile banking

- Internet banking

- SMS

How to withdraw money?

You can withdraw money from your account using the following methods:

- ATM

- Bank branch

- NEFT/RTGS

- IMPS

How to transfer money?

You can transfer money from your account to another account using the following methods:

- NEFT/RTGS

- IMPS

- Cheque

- Demand draft

How to pay bills?

You can pay bills such as electricity, water, and gas using the following methods:

- ATM

- Mobile banking

- Internet banking

- NEFT/RTGS

- IMPS

What are the challenges of PMJDY?

The main challenges of PMJDY include:

- Lack of awareness about the scheme.

- Lack of infrastructure in rural areas.

- Lack of skilled manpower.

- Lack of financial literacy among the poor.

What are the future plans of PMJDY?

The government plans to expand the scope of PMJDY to include more financial services such as credit, insurance, and pensions. The government also plans to make it easier for people to access the benefits of PMJDY by simplifying the application process and reducing the documentation requirements.

Leave a Reply